OPFS money and debt advice service

OPFS’s money and debt advice service provides free, confidential advice for single parents anywhere in Scotland.

Our expert advisers will work with you every step of the way to understand your financial situation, explore all available options for managing your debt and provide support with putting your chosen solutions into action.

Get in touch today

Not enough income to cover essential outgoings?

If you have more money going out than coming in, you need to get support from a free professional money adviser. They can help you improve your financial wellbeing, which will benefit both you and your family in the long-term.

It is not advisable that you try to deal with your debts by yourself.

A money adviser can support you to look at your budget and will assist you to see if you can increase your income or decrease your outgoings. They will advise you on what options you have to deal with your debts. For example, you may need to declare yourself bankrupt so that you can clear your debts and be able to move on.

There are different options for dealing with debt, depending on your circumstances and how much surplus income you have.

To find out which solution might be best for you, take a look at the three options below to see which matches your circumstances the best.

Not enough income to cover essential outgoings

If you’re unable to afford essential outgoings such as bills, food and rent, get advice from a free professional money adviser. It is not advisable that you try to deal with your debts yourself, especially if you’re in a crisis.

More resources for if you are struggling to pay for essentials:

- call our helpline between 9:30am and 4pm Monday to Friday on 0808 801 0323, use our live web chat or email us

- our helpline advisors can do a free benefits check, or you can use the Turn2Us online benefits calculator to find out what benefits you may be entitled to

- access crisis support through one of our local services

- find out how you can reduce your living costs and get support with your fuel costs

- the Scottish Welfare Fund provides help to those in urgent need of money to pay for food, fuel or essential household items

- use our free budgeting and debt planner

No surplus income after essential outgoings are paid

If you have nothing left to offer creditors after essential outgoings have been paid, you will need to carefully consider your options.

Once you have used our Budgeting tool you need to decide if you can afford to offer any of your creditors a payment. Any payments you make will depend on how much you have to offer, how much your total debt is and what debt repayment option is best for you. If you have priority debts to pay, such as Rent arrears, or there is pending court action, it would be in your best interest to get the support of a free professional adviser.

Your credit rating will probably be affected, and it could be difficult for you to get credit in the future.

You could write to your creditors and ask them to put your debt on hold until you think your circumstances will improve. This is called a moratorium. It is only a short-term solution, and your creditors will not hold off indefinitely.

You could also offer a token payment. For example £1.00 per month for a short period of time, you would need to look at your budget to assess whether you can afford this. This would give you a short period of time to look at more long-term solutions with a professional adviser.

Some Surplus Income after essential outgoings have been paid

Once you have used our Budgeting tool you need to decide if you can afford to offer any of your creditors a payment. Any payments you make will depend on how much you have to offer, how much your total debt is and what debt repayment option is best for you. If you have priority debts to pay, such as Rent arrears, or there is pending court action, it would be in your best interest to get the support of a free professional adviser.

Your credit rating will probably be affected, and it could be difficult for you to get credit in the future.

If you decide that you can pay your creditors some money back now, it’s important to contact them as soon as possible.

Contacting your creditors and how much to offer them

Once you know how much you owe each of your creditors, your need to decide how much you can afford to offer them. Look at your completed Budget and Debt List. This will show you what you can afford.

Arrange payments yourself

To arrange payments yourself you will need to decide how much you can offer. Be realistic and don’t offer to pay a certain amount unless you can afford to stick to making these payments. It’s better to offer a smaller amount that you know you can afford, rather than offering a larger amount that you will then default on the first time you are a bit short of money. Any priority debt repayments usually must cover ongoing charges, and add something for the arrears, so keep this in mind.

You can offer creditors the same amount each if you owe similar amounts but if your creditors are owed very different amounts, you would be best to split your surplus income between them on a pro-rata basis (whoever is owed the most gets the biggest share of the surplus amount).

You will see all your debt details on the debt tool screen which you can change as you need to. Once you have these figures you would write to all the creditors with a list of the offer being made. If a creditor is still charging interest, you would ask again that all charges be stopped so that you can repay your debt as soon as possible.

Arranging deductions through your benefits

You could also look at arranging deductions through your benefits for priority debts. For example a set deduction for Council Tax arrears through your Universal Credit. If you arrange this, remember to change the details on the income and expenditure pages. These deductions are a good way to spread your payment at a rate you can afford and they usually stop your creditor acting against you as you maintain your payments.

It can take weeks for creditors to reply to you and some don’t reply at all but will accept your offer. If you have let the creditor know how much you can pay them back, they have 28 days to accept, or you will take it that they agreed. After this time has passed you can go ahead and set up your payments.

Third Party Deductions

If you owe arrears for certain things, you can arrange deductions from your benefit. These deductions are called Third Party Deductions. You can usually arrange these yourself or the people you owe the money to can apply for these deductions.

You can’t have more than three payments deducted and you would need to agreed to having more than 15% of your Personal Allowance taken.

Getting deductions from your benefit to pay arrears can help you budget better as you know exactly how much is being taken and will also have a record of your payments.

Below is a list of the types of arrears that can be deducted:

- housing costs (not previous addresses)

- fuel costs (current provider only)

- Council Tax

- unpaid fines

- water and sewage rates

Below is a list of Benefits than can have deductions taken from them:

- Universal Credit

- Income Support

- Pension Credit

- Job Seekers Allowance

- Employment Support Allowance

Work out how much to pay each creditor

You can offer creditors the same amount each if you owe similar amounts but if your creditors are owed very different amounts, you would be best to split your surplus income between them on a pro-rata basis (whoever is owed the most gets the biggest share of the surplus amount).

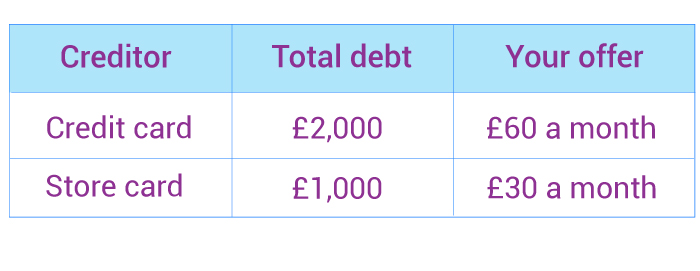

Example

You’ve got 2 debts

You owe money on a credit card and a store card.

How much do you owe on each?

You owe twice as much on the credit card as you do on the store card, so your offer to the credit card company should be twice as much.

What have you got left?

You have £90 left each month to pay off your debts. So you choose to pay back £60 to the credit card each month and the remaining £30 to the store card each month.

Write to your creditors

Write to each creditor with your repayment offer and include a copy of your budget. This will show creditors you’re only spending money on essential living costs and that the offer you’re making is fair.

Make sure you explain how much you can afford to pay each week or month.

Use our sample letter for contacting your creditors.

You can download this template below.

Download Letter for contacting your creditors